Which Of The Following Is Not A Service Provided By Financial Intermediaries?

Chapter 27. Money and Cyberbanking

27.3 The Function of Banks

Learning Objectives

Past the end of this section, you will be able to:

- Explain how banks act equally intermediaries between savers and borrowers

- Evaluate the relationship between banks, savings and loans, and credit unions

- Clarify the causes of bankruptcy and recessions

The belatedly bank robber named Willie Sutton was once asked why he robbed banks. He answered: "That'southward where the money is." While this may have been true at one time, from the perspective of mod economists, Sutton is both right and incorrect. He is wrong because the overwhelming bulk of money in the economic system is not in the course of currency sitting in vaults or drawers at banks, waiting for a robber to appear. Most coin is in the form of bank accounts, which exist simply as electronic records on computers. From a broader perspective, however, the bank robber was more right than he may have known. Banking is intimately interconnected with coin and consequently, with the broader economy.

Banks brand information technology far easier for a complex economy to carry out the boggling range of transactions that occur in goods, labor, and financial capital markets. Imagine for a moment what the economic system would be similar if all payments had to be fabricated in cash. When shopping for a large purchase or going on holiday yous might need to carry hundreds of dollars in a pocket or handbag. Even small businesses would need stockpiles of greenbacks to pay workers and to purchase supplies. A bank allows people and businesses to store this coin in either a checking account or savings account, for example, and then withdraw this money as needed through the use of a direct withdrawal, writing a check, or using a debit menu.

Banks are a critical intermediary in what is chosen the payment organisation, which helps an economic system exchange goods and services for money or other fiscal assets. Also, those with extra money that they would like to relieve tin store their money in a bank rather than look for an private that is willing to borrow it from them and then repay them at a afterwards date. Those who desire to borrow money can go direct to a depository financial institution rather than trying to find someone to lend them cash Transaction costs are the costs associated with finding a lender or a borrower for this money. Thus, banks lower transactions costs and human activity as financial intermediaries—they bring savers and borrowers together. Along with making transactions much safer and easier, banks also play a key office in the creation of coin.

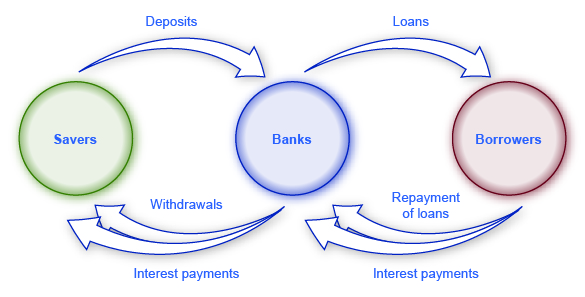

Banks equally Financial Intermediaries

An "intermediary" is one who stands between 2 other parties. Banks are a financial intermediary—that is, an establishment that operates betwixt a saver who deposits money in a bank and a borrower who receives a loan from that bank. Financial intermediaries include other institutions in the financial market such as insurance companies and alimony funds, but they will not be included in this discussion considering they are non considered to be depository institutions, which are institutions that have money deposits and then utilize these to make loans. All the funds deposited are mingled in one big puddle, which is then loaned out. Effigy 1 illustrates the position of banks as financial intermediaries, with deposits flowing into a bank and loans flowing out. Of form, when banks make loans to firms, the banks will endeavor to funnel financial capital letter to salubrious businesses that have adept prospects for repaying the loans, not to firms that are suffering losses and may exist unable to repay.

How are banks, savings and loans, and credit unions related?

Banks accept a couple of close cousins: savings institutions and credit unions. Banks, as explained, receive deposits from individuals and businesses and brand loans with the money.

Savings institutions are also sometimes chosen "savings and loans" or "thrifts." They also take loans and make deposits. However, from the 1930s until the 1980s, federal police force limited how much involvement savings institutions were allowed to pay to depositors. They were also required to make about of their loans in the form of housing-related loans, either to homebuyers or to existent-estate developers and builders.

A credit union is a nonprofit financial institution that its members own and run. Members of each credit wedlock decide who is eligible to be a fellow member. Usually, potential members would be anybody in a certain customs, or groups of employees, or members of a sure organization. The credit spousal relationship accepts deposits from members and focuses on making loans dorsum to its members. While there are more credit unions than banks and more banks than savings and loans, the full assets of credit unions are growing.

In 2008, in that location were 7,085 banks. Due to the banking company failures of 2007–2009 and bank mergers, in that location were 5,571 banks in the U.s. at the end of the fourth quarter in 2014. According to the Credit Union National Clan, every bit of December 2014 there were vi,535 credit unions with avails totaling $1.1 billion. A solar day of "Transfer Your Money" took identify in 2009 out of general public cloy with big bank bailouts. People were encouraged to transfer their deposits to credit unions. This has grown into the ongoing Move Your Money Project. Consequently, some now concur deposits as large as $50 billion. However, as of 2013, the 12 largest banks (0.2%) controlled 69 percent of all banking assets, according to the Dallas Federal Reserve.

A Banking company'due south Balance Sheet

A balance canvass is an bookkeeping tool that lists avails and liabilities. An asset is something of value that is owned and can be used to produce something. For instance, the cash yous ain can be used to pay your tuition. If you lot own a home, this is also considered an nugget. A liability is a debt or something you owe. Many people infringe money to buy homes. In this case, a home is the asset, but the mortgage is the liability. The net worth is the asset value minus how much is owed (the liability). A bank's balance sheet operates in much the aforementioned way. A bank's net worth is also referred to as bank capital. A banking company has avails such equally cash held in its vaults, monies that the bank holds at the Federal Reserve bank (called "reserves"), loans that are made to customers, and bonds.

Figure 2 illustrates a hypothetical and simplified balance sheet for the Safe and Secure Bank. Because of the 2-column format of the residual sheet, with the T-shape formed by the vertical line down the middle and the horizontal line under "Assets" and "Liabilities," it is sometimes called a T-business relationship.

The "T" in a T-account separates the assets of a firm, on the left, from its liabilities, on the right. All firms utilise T-accounts, though near are much more complex. For a bank, the assets are the fiscal instruments that either the bank is holding (its reserves) or those instruments where other parties owe money to the depository financial institution—like loans made by the banking concern and U.South. Government Securities, such as U.South. treasury bonds purchased by the bank. Liabilities are what the bank owes to others. Specifically, the bank owes any deposits made in the bank to those who have made them. The net worth of the banking company is the total assets minus total liabilities. Net worth is included on the liabilities side to have the T account residuum to zero. For a healthy business, net worth will be positive. For a bankrupt firm, internet worth will be negative. In either case, on a bank's T-account, assets will always equal liabilities plus internet worth.

When banking concern customers deposit money into a checking account, savings account, or a certificate of deposit, the bank views these deposits equally liabilities. After all, the bank owes these deposits to its customers, when the customers wish to withdraw their coin. In the example shown in Figure 2, the Safe and Secure Bank holds $10 meg in deposits.

Loans are the first category of bank assets shown in Figure 2. Say that a family unit takes out a xxx-twelvemonth mortgage loan to purchase a house, which ways that the borrower will repay the loan over the adjacent 30 years. This loan is clearly an asset from the bank's perspective, considering the borrower has a legal obligation to make payments to the bank over time. But in practical terms, how tin the value of the mortgage loan that is being paid over 30 years be measured in the present? One fashion of measuring the value of something—whether a loan or anything else—is by estimating what some other party in the market is willing to pay for it. Many banks issue habitation loans, and accuse various handling and processing fees for doing so, but and so sell the loans to other banks or financial institutions who collect the loan payments. The market place where loans are made to borrowers is called the master loan marketplace, while the marketplace in which these loans are bought and sold by financial institutions is the secondary loan marketplace.

I key factor that affects what financial institutions are willing to pay for a loan, when they buy it in the secondary loan market, is the perceived riskiness of the loan: that is, given the characteristics of the borrower, such every bit income level and whether the local economy is performing strongly, what proportion of loans of this type will exist repaid? The greater the risk that a loan will not be repaid, the less that any financial establishment will pay to acquire the loan. Another cardinal gene is to compare the interest rate charged on the original loan with the current interest rate in the economic system. If the original loan made at some point in the past requires the borrower to pay a low interest rate, but electric current involvement rates are relatively high, and then a financial establishment will pay less to learn the loan. In contrast, if the original loan requires the borrower to pay a high interest rate, while electric current involvement rates are relatively low, and then a financial establishment will pay more to learn the loan. For the Safe and Secure Bank in this case, the full value of its loans if they were sold to other fiscal institutions in the secondary market is $5 million.

The second category of bank asset is bonds, which are a common mechanism for borrowing, used by the federal and local regime, and also private companies, and nonprofit organizations. A bank takes some of the money information technology has received in deposits and uses the coin to buy bonds—typically bonds issued by the U.S. government. Government bonds are depression-risk considering the government is nearly sure to pay off the bond, admitting at a low charge per unit of interest. These bonds are an asset for banks in the same way that loans are an asset: The banking company will receive a stream of payments in the futurity. In our example, the Safe and Secure Banking company holds bonds worth a total value of $iv one thousand thousand.

The last entry under assets is reserves, which is money that the bank keeps on hand, and that is not loaned out or invested in bonds—and thus does non lead to interest payments. The Federal Reserve requires that banks keep a certain percentage of depositors' money on "reserve," which means either in their vaults or kept at the Federal Reserve Banking company. This is chosen a reserve requirement. (Budgetary Policy and Bank Regulation volition explain how the level of these required reserves are 1 policy tool that governments have to influence bank behavior.) Additionally, banks may besides want to keep a sure amount of reserves on hand in excess of what is required. The Safe and Secure Banking concern is holding $2 million in reserves.

The net worth of a bank is defined equally its full assets minus its total liabilities. For the Safe and Secure Depository financial institution shown in Figure 2, internet worth is equal to $1 one thousand thousand; that is, $11 1000000 in assets minus $10 million in liabilities. For a financially salubrious banking company, the net worth will be positive. If a banking concern has negative net worth and depositors tried to withdraw their money, the bank would not be able to requite all depositors their money.

For some concrete examples of what banks do, watch this video from Paul Solman'due south "Making Sense of Financial News."

How Banks Become Bankrupt

A banking company that is bankrupt will have a negative net worth, pregnant its assets volition exist worth less than its liabilities. How can this happen? Over again, looking at the residuum canvass helps to explicate.

A well-run bank will assume that a small percentage of borrowers will not repay their loans on time, or at all, and factor these missing payments into its planning. Recollect, the calculations of the expenses of banks every year includes a factor for loans that are not repaid, and the value of a depository financial institution's loans on its balance canvass assumes a certain level of riskiness because some loans will not be repaid. Even if a bank expects a certain number of loan defaults, it volition suffer if the number of loan defaults is much greater than expected, as can happen during a recession. For case, if the Safe and Secure Bank in Figure two experienced a wave of unexpected defaults, so that its loans declined in value from $5 million to $3 million, and so the avails of the Safety and Secure Bank would turn down and so that the depository financial institution had negative net worth.

What led to the financial crisis of 2008–2009?

Many banks brand mortgage loans so that people can buy a home, only then do not keep the loans on their books as an nugget. Instead, the bank sells the loan. These loans are "securitized," which means that they are bundled together into a financial security that is sold to investors. Investors in these mortgage-backed securities receive a charge per unit of return based on the level of payments that people make on all the mortgages that stand behind the security.

Securitization offers certain advantages. If a banking concern makes most of its loans in a local area, and then the bank may be financially vulnerable if the local economy declines, and then that many people are unable to make their payments. Just if a bank sells its local loans, and then buys a mortgage-backed security based on domicile loans in many parts of the country, it can avoid being exposed to local financial risks. (In the simple example in the text, banks just own "bonds." In reality, banks can ain a number of financial instruments, as long as these fiscal investments are safe enough to satisfy the regime bank regulators.) From the standpoint of a local homebuyer, securitization offers the benefit that a local banking company does not demand to have lots of extra funds to make a loan, because the bank is just planning to concur that loan for a curt time, earlier selling the loan and then that it can be pooled into a financial security.

Simply securitization also offers one potentially large disadvantage. If a bank is going to hold a mortgage loan equally an asset, the bank has an incentive to scrutinize the borrower carefully to ensure that the loan is likely to be repaid. However, a bank that is going to sell the loan may be less careful in making the loan in the outset identify. The bank will be more than willing to brand what are called "subprime loans," which are loans that have characteristics similar low or zero downward-payment, piddling scrutiny of whether the borrower has a reliable income, and sometimes low payments for the get-go year or two that will exist followed by much higher payments after that. Some subprime loans made in the mid-2000s were later dubbed NINJA loans: loans made even though the borrower had demonstrated No Income, No Job, or Assets.

These subprime loans were typically sold and turned into financial securities—just with a twist. The idea was that if losses occurred on these mortgage-backed securities, sure investors would agree to take the first, say, five% of such losses. Other investors would agree to accept, say, the adjacent 5% of losses. By this arroyo, all the same other investors would not need to take any losses unless these mortgage-backed financial securities lost 25% or 30% or more of their total value. These circuitous securities, along with other economic factors, encouraged a big expansion of subprime loans in the mid-2000s.

The economic stage was now set for a banking crisis. Banks idea they were buying just ultra-prophylactic securities, because even though the securities were ultimately backed by risky subprime mortgages, the banks only invested in the part of those securities where they were protected from small-scale or moderate levels of losses. Simply as housing prices barbarous afterwards 2007, and the deepening recession made information technology harder for many people to make their mortgage payments, many banks found that their mortgage-backed financial assets could end upward beingness worth much less than they had expected—so the banks were staring bankruptcy in the face up. In the 2008–2011 period, 318 banks failed in the United States.

The risk of an unexpectedly high level of loan defaults tin be especially difficult for banks considering a bank'due south liabilities, namely the deposits of its customers, tin can be withdrawn quickly, only many of the banking concern's avails like loans and bonds will only be repaid over years or even decades.This nugget-liability time mismatch—a bank'due south liabilities can be withdrawn in the curt term while its assets are repaid in the long term—can cause severe issues for a banking concern. For example, imagine a depository financial institution that has loaned a substantial corporeality of money at a certain interest rate, only then sees interest rates ascension substantially. The bank can observe itself in a precarious state of affairs. If information technology does not heighten the interest rate information technology pays to depositors, so deposits volition flow to other institutions that offering the higher interest rates that are at present prevailing. Nevertheless, if the depository financial institution raises the interest rates that it pays to depositors, it may terminate up in a state of affairs where information technology is paying a college interest rate to depositors than it is collecting from those past loans that were made at lower interest rates. Clearly, the bank cannot survive in the long term if it is paying out more in involvement to depositors than it is receiving from borrowers.

How tin can banks protect themselves against an unexpectedly high rate of loan defaults and against the take chances of an asset-liability time mismatch? One strategy is for a banking company to diversify its loans, which means lending to a variety of customers. For example, suppose a bank specialized in lending to a niche market—say, making a loftier proportion of its loans to construction companies that build offices in one downtown area. If that i surface area suffers an unexpected economic downturn, the bank volition endure large losses. However, if a depository financial institution loans both to consumers who are ownership homes and cars and also to a wide range of firms in many industries and geographic areas, the banking concern is less exposed to risk. When a banking company diversifies its loans, those categories of borrowers who have an unexpectedly large number of defaults volition tend to be balanced out, co-ordinate to random hazard, past other borrowers who have an unexpectedly low number of defaults. Thus, diversification of loans can assistance banks to continue a positive internet worth. However, if a widespread recession occurs that touches many industries and geographic areas, diversification will not help.

Forth with diversifying their loans, banks have several other strategies to reduce the risk of an unexpectedly big number of loan defaults. For instance, banks can sell some of the loans they make in the secondary loan market, equally described earlier, and instead hold a greater share of assets in the form of government bonds or reserves. Yet, in a lengthy recession, most banks will meet their internet worth decline considering a higher share of loans will not exist repaid in tough economic times.

Key Concepts and Summary

Banks facilitate the utilize of money for transactions in the economic system because people and firms tin apply bank accounts when selling or ownership goods and services, when paying a worker or being paid, and when saving coin or receiving a loan. In the financial upper-case letter market, banks are fiscal intermediaries; that is, they operate between savers who supply financial upper-case letter and borrowers who need loans. A rest sheet (sometimes called a T-account) is an accounting tool which lists assets in one column and liabilities in some other column. The liabilities of a banking company are its deposits. The assets of a depository financial institution include its loans, its ownership of bonds, and its reserves (which are non loaned out). The cyberspace worth of a bank is calculated by subtracting the bank's liabilities from its assets. Banks run a risk of negative cyberspace worth if the value of their avails declines. The value of assets tin can pass up because of an unexpectedly loftier number of defaults on loans, or if involvement rates rise and the banking concern suffers an asset-liability time mismatch in which the bank is receiving a low charge per unit of interest on its long-term loans but must pay the currently higher market rate of interest to attract depositors. Banks tin can protect themselves confronting these risks by choosing to diversify their loans or to hold a greater proportion of their avails in bonds and reserves. If banks concur only a fraction of their deposits as reserves, and then the process of banks' lending coin, those loans existence re-deposited in banks, and the banks making additional loans will create money in the economy.

Cocky-Bank check Questions

Explain why the money listed under assets on a depository financial institution remainder sheet may not actually be in the depository financial institution?

Review Questions

- Why is a bank called a financial intermediary?

- What does a rest canvas testify?

- What are the avails of a bank? What are its liabilities?

- How do you summate the internet worth of a bank?

- How can a bank end up with negative internet worth?

- What is the asset-liability time mismatch that all banks face?

- What is the risk if a bank does not diversify its loans?

Critical Thinking Questions

Explain the difference between how you would characterize bank deposits and loans equally assets and liabilities on your own personal residue sheet and how a bank would characterize deposits and loans every bit assets and liabilities on its remainder sail.

Problems

A bank has deposits of $400. Information technology holds reserves of $50. It has purchased government bonds worth $lxx. It has made loans of $500. Prepare up a T-account residue canvas for the bank, with avails and liabilities, and calculate the banking company'due south net worth.

References

Credit Union National Association. 2014. "Monthly Credit Matrimony Estimates." Last accessed March iv, 2015. http://www.cuna.org/Research-And-Strategy/Credit-Marriage-Data-And-Statistics/.

Dallas Federal Reserve. 2013. "Ending `Too Big To Fail': A Proposal for Reform Before Information technology's Too Tardily". Accessed March 4, 2015. http://www.dallasfed.org/news/speeches/fisher/2013/fs130116.cfm.

Richard Westward. Fisher. "Catastrophe 'Besides Big to Fail': A Proposal for Reform Earlier It's Besides Late (With Reference to Patrick Henry, Complexity and Reality) Remarks before the Committee for the Republic, Washington, D.C. Dallas Federal Reserve. Jan 16, 2013.

"Commercial Banks in the U.S." Federal Reserve Banking company of St. Louis. Accessed November 2013. http://research.stlouisfed.org/fred2/series/USNUM.

Glossary

- asset

- item of value endemic by a business firm or an private

- asset–liability time mismatch

- a depository financial institution's liabilities can be withdrawn in the brusque term while its avails are repaid in the long term

- balance sheet

- an accounting tool that lists avails and liabilities

- banking concern capital

- a bank's net worth

- depository institution

- institution that accepts money deposits and then uses these to make loans

- diversify

- making loans or investments with a diverseness of firms, to reduce the risk of beingness adversely affected by events at ane or a few firms

- financial intermediary

- an institution that operates between a saver with financial assets to invest and an entity who will borrow those assets and pay a rate of return

- liability

- whatsoever amount or debt owed past a business firm or an individual

- net worth

- the backlog of the asset value over and to a higher place the corporeality of the liability; full assets minus total liabilities

- payment system

- helps an economy exchange appurtenances and services for money or other financial avails

- reserves

- funds that a bank keeps on hand and that are non loaned out or invested in bonds

- T-account

- a balance canvas with a two-column format, with the T-shape formed by the vertical line downwards the heart and the horizontal line under the column headings for "Avails" and "Liabilities"

- transaction costs

- the costs associated with finding a lender or a borrower for money

Solutions

Answers to Cocky-Check Questions

A bank's assets include greenbacks held in their vaults, just assets also include monies that the bank holds at the Federal Reserve Bank (called "reserves"), loans that are made to customers, and bonds.

Source: https://opentextbc.ca/principlesofeconomics/chapter/27-3-the-role-of-banks/

Posted by: longprajectow.blogspot.com

0 Response to "Which Of The Following Is Not A Service Provided By Financial Intermediaries?"

Post a Comment